Credit Cards4 min read

Interest Charges Become The First Bill To Attack In 2026

Bill Hardekopf · December 29, 2025

A household looking for a clear 2026 target should start with the balances charging the most interest.

Year archive

Browse the 2025 BillSaver archive for consumer-money articles on credit cards, banking, insurance, travel, taxes, utilities, and everyday bills.

Year archive

A household looking for a clear 2026 target should start with the balances charging the most interest.

The final Monday of 2025 is a good day to build the 2026 budget around paydays and due dates.

The end of 2025 is a good time to compare deductibles with the cash the household could actually reach.

The Federal Reserve cut rates in December 2025, but household debt still needed account-by-account review.

Holiday balances heading into 2026 need a payoff date before they become ordinary debt.

Year-end 2025 tax planning still required receipts, charitable records, clean-energy paperwork, and withholding checks.

The most honest subscription audit starts with the card statement, not memory.

Unused travel credits, vouchers, and card benefits can disappear if nobody tracks expiration dates.

The end of 2025 is a good time to compare deductibles with cash that could actually be used.

Giving Tuesday appeals can be real and urgent, but fake links and lookalike names still deserve suspicion.

Holiday travel cards should be chosen for protections, fees, refund rules, and payoff timing before rewards enter the conversation.

Year-end tax planning is easier when charitable receipts, energy-credit documents, business records, and withholding notes are in one place.

Family help can be generous and still put the giver's budget at risk.

Giving Tuesday appeals work best when generosity is paired with simple verification.

Helping family can be right and still require a limit that protects rent, food, savings, and debt payments.

Buy now, pay later offers can make holiday purchases feel smaller by moving the pain into later weeks.

Buy now, pay later offers can create several small due dates that collide with rent, utilities, and card bills.

Holiday shopping in 2025 met card APRs that made every carried balance more expensive.

Holiday shopping in 2025 still needed to respect credit card APRs before rewards, points, or limited-time deals.

Open enrollment for 2026 benefits required a fresh look at premiums, deductibles, prescriptions, and worst-case cash needs.

Medicare Part D changes for 2026 made prescription costs a budget item worth checking before the new year.

Medicare open enrollment is the yearly moment to compare prescriptions, pharmacies, premiums, and plan rules.

The Education Department announced the 2026-27 FAFSA was available earlier than the traditional deadline.

Medicare open enrollment is the annual chance to compare prescriptions, pharmacies, premiums, and plan rules.

The September 2025 Fed meeting gave households another reason to compare savings yields and variable debt costs.

Open enrollment for 2026 benefits should start with expected care and cash reserves, not loyalty to last year's plan.

September budgets had to handle rate headlines without pretending every household debt would improve at the same speed.

Credit reports deserve a fall review before new loans, leases, cards, and holiday financing enter the picture.

Payment apps are ordinary household tools, but linked accounts, instant transfers, and privacy settings still deserve a review.

Labor Day auto promotions can make buyers think about monthly payments before insurance, repairs, and total interest.

Labor Day auto promotions can make monthly payments look manageable before insurance, taxes, and repairs are priced.

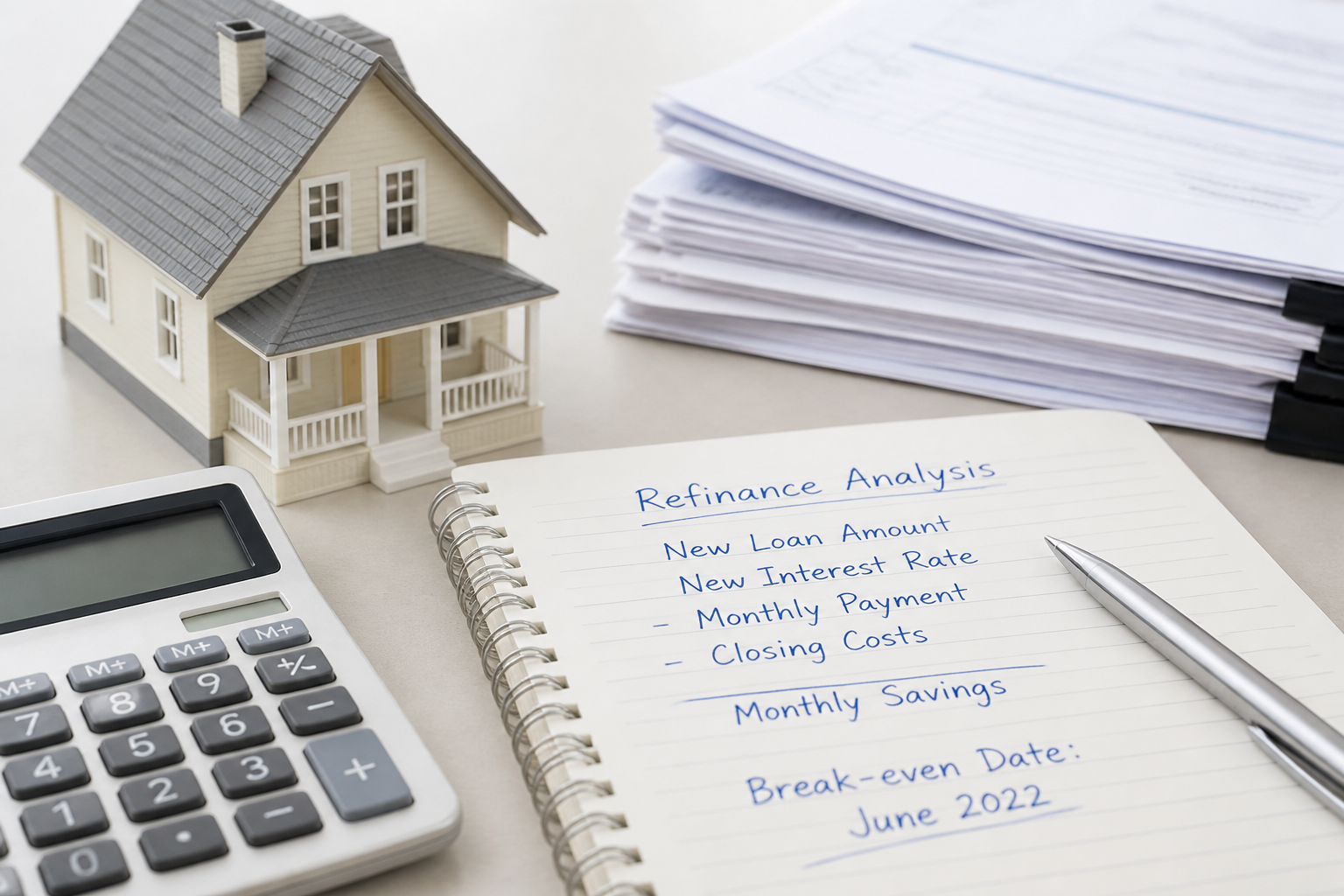

Lower-rate hopes brought refinance ads back into view, but homeowners still needed break-even math.

The FAFSA calendar works better when families handle logins and contributor access before school deadlines start piling up.

The Education Department opened a beta path for the 2026-27 FAFSA in August 2025, moving financial-aid preparation earlier.

Parents adding students as authorized users should set rules before the card is needed on campus.

Late-summer apartment moves can stack application fees, deposits, utility setup charges, and moving costs in the same month.

Parents who send students to campus with authorized user cards should not rely on vague instructions.

Late-summer apartment deposits, utility setup fees, and moving costs can hit before the semester or lease budget is ready.

Auto insurance renewals can change enough to deserve a fresh comparison instead of an automatic payment.

College move-in brings checking accounts, payment apps, parent transfers, card alerts, and emergency money into daily use.

Students heading to campus need payment app rules as much as checking account access.

Midyear statements can show whether interest charges are eating more of the budget than rewards are giving back every month.

Back-to-school spending in 2025 could blend required supplies with devices, apps, subscriptions, and accessories.

Prime Day 2025 was announced as a four-day event, making one-click buying and saved cards even easier to overuse.

The June 2025 Fed meeting kept variable-rate borrowing and home equity lines in the same conversation.

Storm season is a practical time to ask whether the household could actually pay the deductible it chose.

Homebuyers still needed a payment range that worked without betting on perfect rates.

Mortgage loans can be sold or transferred without changing the loan terms, but the payment routine still needs attention.

The first hot bills of the year are a good time to separate higher usage from higher rates.

Wedding season is a useful moment to clear up myths about joint accounts, authorized users, and shared debt.

Holiday-weekend travel can make hotel holds, rental-car deposits, baggage fees, and gas purchases hit at once.

Auto insurance renewals in 2025 gave households another recurring bill worth shopping carefully.

Spring and summer trials can quietly become real subscriptions once the family calendar gets busy.

Spring storm season is a reminder that the premium is only one part of the real insurance decision.

Borrowers with student loan payments back in the budget needed to test whether summer spending was crowding out the due date.

Summer travel cards can help with protections and rewards, but only if the trip is paid off quickly.

Before hurricane season, households had time to review wind, flood, and named-storm deductibles before weather turned urgent.

Federal student loan borrowers in 2025 still needed to rebuild payment habits after the pandemic pause and on-ramp period.

Summer travel cards can help with protections and rewards, but fees and payoff timing still decide whether the trip fits.

Families comparing college offers in 2025 needed to look beyond freshman-year aid and sticker-price excitement.

Taxpayers short on cash near the April deadline could solve one problem with a card and accidentally create a more expensive one.

Families comparing college offers in 2025 had to account for tuition, housing, food, travel, fees, and borrowing costs.

Energy credits can help, but households still need eligibility, receipts, and payback math before financing a project.

Energy credits kept home upgrades in the conversation in 2025, but paperwork and payback still mattered.

The April 15 deadline still required taxpayers who owed money to separate filing from payment strategy.

Federal Reserve meetings in 2025 kept savings yields, mortgage rates, and card APRs in the same household conversation.

Borrowers with federal student loans in repayment needed to make sure the payment plan still fit income and family size.

Medical credit offers can show up when families are already stressed and trying to say yes to care.

Spring break travel can scatter card use across gas stations, hotels, rental counters, apps, and airport purchases.

As the 2025 spring market opened, homebuyers still needed affordability math that worked without assuming rates would fall on schedule.

As the 2025 spring market approached, buyers had to think about monthly comfort before chasing a quoted mortgage rate.

Wireless bills can carry old lines, device plans, insurance, and add-ons long after the household stopped noticing them.

Presidents Day auto ads in 2025 still leaned on monthly payments while buyers faced high financing and insurance costs.

Car buyers in 2025 needed to price insurance before letting a monthly payment define affordability.

Shared credit cards, authorized users, and recurring subscriptions work better when the payoff agreement is written before spending starts.

Shared cards, shared rent, and shared subscriptions work best when both people can see the bill before it becomes a balance.

The Federal Reserve held rates steady in January 2025, leaving borrowers to manage costs that were still high at home.

The 2025 filing season made refund timing tempting to treat as guaranteed money, especially for households already juggling winter bills.

Tax refund season can help, but one deposit should not carry the entire savings plan for 2025.

As tax forms began arriving, refund expectations were less useful than a sober look at paycheck withholding and credits.

High credit card balances and delinquency concerns kept consumer stress in the news in early 2025.

January wireless bills can reveal promotions that expired, device payments that lingered, and add-ons nobody meant to keep.

The IRS announced a January 27 opening for the 2025 filing season, giving taxpayers a clear starting point for 2024 returns.

January 2025 medical-debt credit reporting news was about to put credit reports and old medical bills back in front of households.

The first week of 2025 called for a budget that admitted how long higher prices, higher rates, and larger minimum payments had been hanging around.